Class Distinctions & Income Brackets

This resource will help you identify your class experience(s).

Class is a system of power based on perceived social and economic status. While closely connected, class and money are not the same thing. The class we are raised in strongly shapes our values, beliefs, and expectations. These imprints can deeply inform ways of thinking and acting throughout life. For most people, the class we are raised in is the primary determining factor of what economic bracket we will stay within. Class is a much more fixed (less mobile) category than dominant narratives in the United States would have us believe. The majority of people in the U.S. have limited or no class mobility. However, some people experience upward or downward class mobility and an associated range of different life experiences. And some people grow up in mixed-class households and have different class patterns and norms demonstrated or modeled on different sides of their family.

For Resource Generation’s work, we believe that internalized class privilege has strong staying power for upper-class people who are downwardly mobile and that internalized privilege also appears quickly for people who are newly wealthy.

Here are some examples of this:

- A person from wealth with multiple degrees and no student loans who has gone bankrupt

- This person is in the bottom economic bracket but still has the safety net and privileges of being raised owning-class.

- A person who grew up working-class who, as determined by their income/salary, is among the top 10% highest paid people in the U.S.

- Though they do not have the same lifetime of social training as someone raised in the upper-class, money offers this person access to certain spaces and power; they will begin to internalize class privilege.

- A middle or upper-class person who works a low-paying job (i.e., barista, non-profit)

- Compared to a poor or working-class person, it’s more likely that working a low-paying job is their choice rather than one of necessity. This person might experience economic insecurity, but they will retain the privileges that allow them to make more money, change careers in the future, and might be able to access their family’s safety net throughout their lifetime.

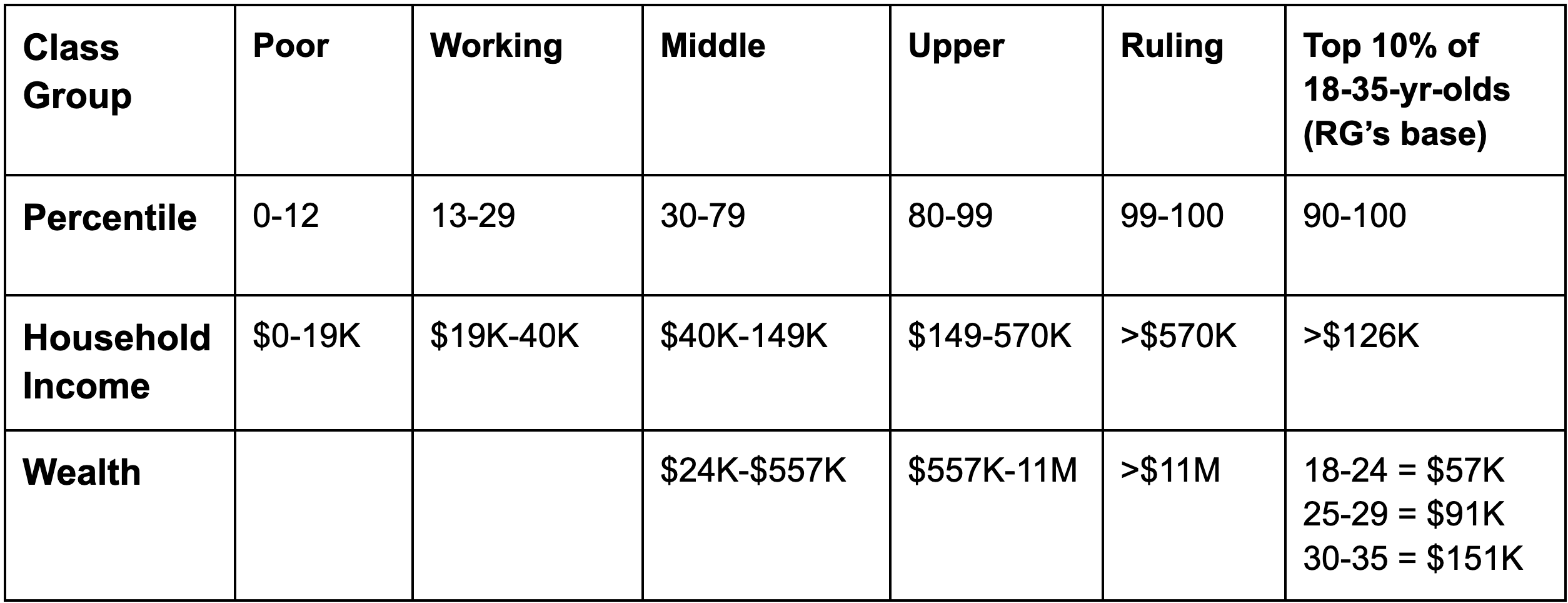

Please use the guide to help locate yourself and your family. These numbers are based in the U.S., some international perspective can be found here.

Poor and Working-Poor

- Life experience often marked by:

- Substandard, unstable or inconsistent housing

- Underemployed/underpaid, sometimes long-term use of public benefits

- Little access to higher education

- Basic living expenses might be impossible/difficult to obtain

- Debt from predatory lending services (cash advance, etc.), monthly bills, or emergencies

- Chronic lack of health care, food, or other necessities

- Frequent involuntary moves, chaos, and disruption of life

- Often raised with strong values on resource sharing and caretaking

- Targeted and incarcerated disproportionately by the state generally and specifically through systems like child protective services, vagrancy laws, immigration enforcement, and money/cash bail

- Intellectual, artistic, and labor contributions frequently co-opted and made invisible in dominant society

- Treated as disposable. Conditioned away from participating in the dominant society.

- Approximately 12% of the U.S. population, but overwhelmingly have negative assets and thus combined represent -1% of U.S. total net wealth.

- Not positioned as political or economic decision-makers. Often scapegoated and labeled as a burden on society.

Working-Class

- Life experience often marked by:

- Housing is sometimes unstable. Rental housing, or if owning a home, the majority of assets and potential for wealth are tied to it.

- Occupation often involves physical labor, service, or care work for upper and middle-class people. Little control over pay, hours, or access to benefits.

- Access to higher education is spotty, a large amount of student debt common for people who attend 4-year universities

- Generally living paycheck to paycheck with little or no savings

- Debt from education, medical bills, and credit cards from day-to-day living expenses or emergencies

- Might include turning to public (or community) safety nets to help make ends meet

- Often raised with strong value on resource sharing and taking care of each other

- Targeted by the state as a huge source of revenue through fines, fees, and cash/money bail

- Treated as replaceable. Conditioned to resent middle-class professionals (such as bosses, lawyers) and toward the idealization of wealth

- Approximately 35% of the population controls roughly 4% of the U.S. total net wealth.

- Not positioned as political or economic decision-makers. White working-class are scapegoated as the reason for regressive politics, and working-class people of color are ignored.

Middle-Class

- Life experience often marked by:

- Homeownership or other generally stable housing

- Depends on wages/salaries to pay the bills. Often jobs with some benefits, some control over the hours and methods of work and/or control over others’ work

- Social status and social connections to help the next generation

- College generally expected, may or may not complete Bachelor’s degree

- Debt is most often in mortgages, education, medical bills

- Can generally expect to hold stable employment, but status can become precarious when there are unexpected expenses such as high medical bills, loss of pensions or layoffs

- Class confusion, especially in association with managerial/upper-class people who incorrectly self-identify as middle-class

- Often at low risk for state interventions with limited ability to seek legal aid if needed

- Treated as the norm. Conditioned toward fear of being poor and to act in allegiance with, and aspire to be upper-class.

- Approximately 32% of the population controls roughly 12% of the U.S. total net wealth.

- Sometimes positioned as political and economic decision-makers and regarded as an important demographic.

Managerial/Upper-Class

- Life experience often marked by:

- Owning one or multiple homes, travel (including international)

- Dependent on salaries, not investments, to pay bills — mid-level to high-level managerial or professional jobs

- Education at elite/selective colleges or at public universities often without student loans

- Some investment in stock market, might have enough savings to retire early

- Might receive or pass down significant inheritances

- Social connections, status, and financial knowledge to help the next generation remain financially well-off

- Generally at low risk for state interventions, often know legal loopholes, and can turn to private legal aid as needed

- Treated as experts. Conditioned towards comparing up so as to see themselves as not that wealthy.

- Approximately 20% of the population controls roughly 53% of the U.S. total net wealth.

- Frequently positioned as political and economic decision-makers and as central actors in shaping national narratives.

Owning/Ruling-Class

- Life experience often marked by:

- Owning luxurious home or homes, travel (including international)

- Enough income from assets (stocks, bonds, etc.) that full-time work is optional

- Education at elite/selective private schools and elite colleges without student loans

- Receiving and/or passing down large inheritances

- Social connections, status, and financial knowledge to help the next generation remain wealthy

- Often encouraged towards hyper-individualism resulting in isolation.

- Usually at low risk for state interventions, know/create legal loopholes, and can call on top legal aid as needed

- Treated as leaders. Conditioned towards seeing poverty as an individual’s fault and wealth as a result of an individual’s accomplishment/”hard work.”

- Ruling-class describes people who are in the global elite and hold the vast majority of power to determine conditions of people’s lives: billionaires, major CEOs, presidents, senators, or other high positions of state power (i.e., any cabinet position in a presidential administration), oligarchs, etc.

- Approximately 1% of the population controls roughly 32% of U.S. total net wealth.

- Positioned as political and economic decision-makers and central actors in shaping reality for self and others.

*Wealth is what you own minus what you owe.

At Resource Generation, we organize young people (18-35 years old) with access to current or future wealth through family or a high income in the top 10% of the U.S. economy. Think you might fall into the top 10% and want to be a member of Resource Generation? Take our class privilege quiz.